When working with clients on the topic of their credit score, I have found there are a handful of questions that are often brought up. So today, I wanted to share with you the eight facts you need to know.

Understanding how your credit works is crucial to building and maintaining a healthy score. It’s sometimes difficult to know the facts when lots of outdated (and incorrect) credit advice tends to linger. It’s no wonder some of us are lost and don’t know where to start when it comes to managing credit.

1. Your credit score is based on five core factors.

Five factors impact your FICO score and each criterion accounts for varying percentages of your credit score. These factors are essential to keep in mind when applying and using credit. Some myths, like carrying a balance to improve your score, can actually damage your score and increase unnecessary debt if you don’t know the real facts. Take a look below at the five factors that impact your credit score.

- 35% – Payment History. Your ability to consistently make payments makes the most significant impact on your score. Late and missed payments are the most detrimental to you.

- 30% – Credit Utilization. This is the next most impactful aspect. Credit utilization is determined by the amount of credit you’re using compared to the total credit you have available. The lower your credit utilization, the better your score.

- 15% – Length of Credit History. Credit history takes a smaller but still important role in influencing your credit score. A longer credit history gives the credit bureaus a bigger snapshot of your past transactions.

- 10% – Inquiries and New Credit. The number of formal requests (known as inquiries) to review your credit report affects your score as well.

- 10% – Diversification of Credit. Lastly, the diversity of your credit types makes up the last area that impacts your credit score. A diverse credit portfolio benefits you since it demonstrates your ability to manage different credit types successfully.

2. FICO credit scores range from 300 to 850.

Scores ranges vary depending on the credit bureau. Knowing your score can help you understand how you can improve it. For example, if you’re looking to move from “fair” to “good,” it’s important to know where those scores lie on the spectrum. Below you can find the credit ranges used by FICO.

- 800–850: Exceptional

- 740–799: Very Good

- 670–739: Good

- 580–669: Fair

- 300–579: Poor

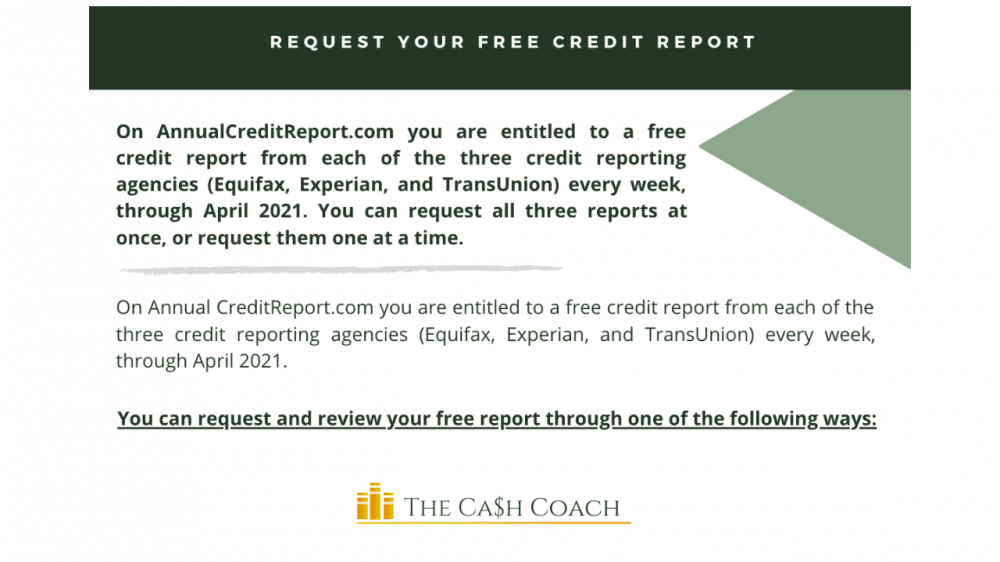

Here are directions you can use to request your free credit report.

3. You have many different credit scores.

You may have a different score with each of the three nationwide credit reporting agencies (TransUnion, Equifax and Experian). Don’t be worried if that’s the case. They all collect similar information, and a lot of it overlaps, but scores can vary for several reasons. For example, lenders can choose to report to one, two or all three agencies. Because of this, the information in your reports can vary, which is partly why your scores can differ too.

4. Checking your own score won’t hurt your score.

Many believe that checking your score hurts your credit, but this is not true. Ordering your credit report or checking your score (called “soft” inquiries) does not affect your credit score. Hard inquiries, like when lenders look at your credit, do negatively impact your score. However, the consequences are small and temporary, especially if the queries are made close together within a short amount of time.

5. Yes, the rumor is true; canceling old cards can lower your score.

The length of your credit history makes up 10 percent of your credit history. Keeping old cards open will positively impact your score since they increase your overall credit age. Having open credit cards also impacts your utilization. All open cards contribute to and raise your overall credit limit. The higher your limit, the easier it is to keep your credit utilization ratio down.

This is crucial since credit utilization is the second most important factor that impacts your credit score. Closing a really old credit card or a card with a high limit can drastically drop your score. If you need to cancel a card, consider raising the limit on another card to keep your utilization ratio similar.

6. Negative credit items will eventually come off your credit report.

Most negative items will remain on your report for seven years at the most due to the regulations set by the Fair Credit Reporting Act.

7. Your credit report can help you spot fraud.

Periodically checking your credit report allows you to spot fraudulent activity.

8. Many credit reports contain inaccurate credit information.

The Federal Trade Commission found in a study that one in five people has an error on at least one of their credit reports. This is why you should frequently check your credit report and dispute any inaccurate information you find. These inaccuracies can greatly impact your score, depending on the error. For example, one wrongfully reported late payment could drastically drop your score since payment history impacts 30 percent of your credit score.