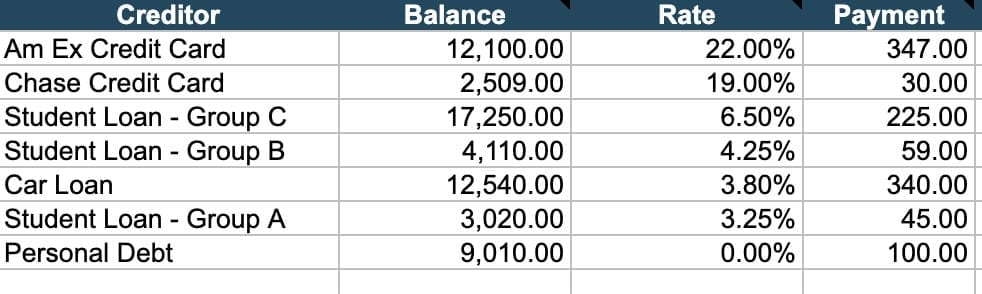

For example, if you determine that the Snowball Method is the best for you, you would be making payments towards your smallest debt first. Let’s say it’s 1K. If the minimum payment is $50, you will add your additional $200 towards this debt each month, making your monthly payments $250. After 4 months, when your 1K debt is paid off, take that $250 you are now used to paying each month and roll it over into making payments on your next debt. If your next debt is 10K and your minimum payment is $500 a month, you add the $250 from the first debt now making your monthly payments $750.